Author: Joel Grewe

I hope that by the time you read this, you’ve already finished filing your taxes. After all, as of publishing, the deadline has just passed. About half of all Americans file their own taxes each year, many relying on software to guide them through the process. I’m one of them. And if you filed this year and claimed dependent children, you likely noticed an increase in the child tax credit compared to last year.

Prior Success

That increase wasn’t accidental. The credit was adjusted to recover value lost to inflation and is now indexed accordingly, meaning it will rise as inflation rises. It’s a simple but meaningful fix that ensures the credit won’t steadily lose its impact over time. Of course, we can still debate whether the amount is sufficient. Anyone raising children, especially multiple children, knows just how expensive that responsibility can be.

But while Congress has taken steps to strengthen support for families through the child tax credit, there’s another part of the tax code that deserves attention: the Child and Dependent Care Credit (CDCC).

What the CDCC is

The CDCC is designed to help offset childcare costs. However, it explicitly excludes what many would consider a traditional family arrangement—where one parent works outside the home, and the other stays home to care for the children.

For those unfamiliar with the credit, here’s a brief overview. The CDCC covers between 20% and 35% of qualifying care expenses, up to $3,000 for one dependent or $6,000 for two or more. There are a few key requirements: the care must be paid to someone other than your spouse (or a child under 19), and the expenses must be incurred so you can work or look for work.

At first glance, the policy seems straightforward. But it also reveals an underlying assumption: childcare needs only arise when both parents are in the workforce. In effect, the tax code nudges families toward a dual-income model by offering support only under those conditions.

Assumptions are wrong

Well… this doesn’t make sense

That assumption no longer reflects the reality of modern family life.

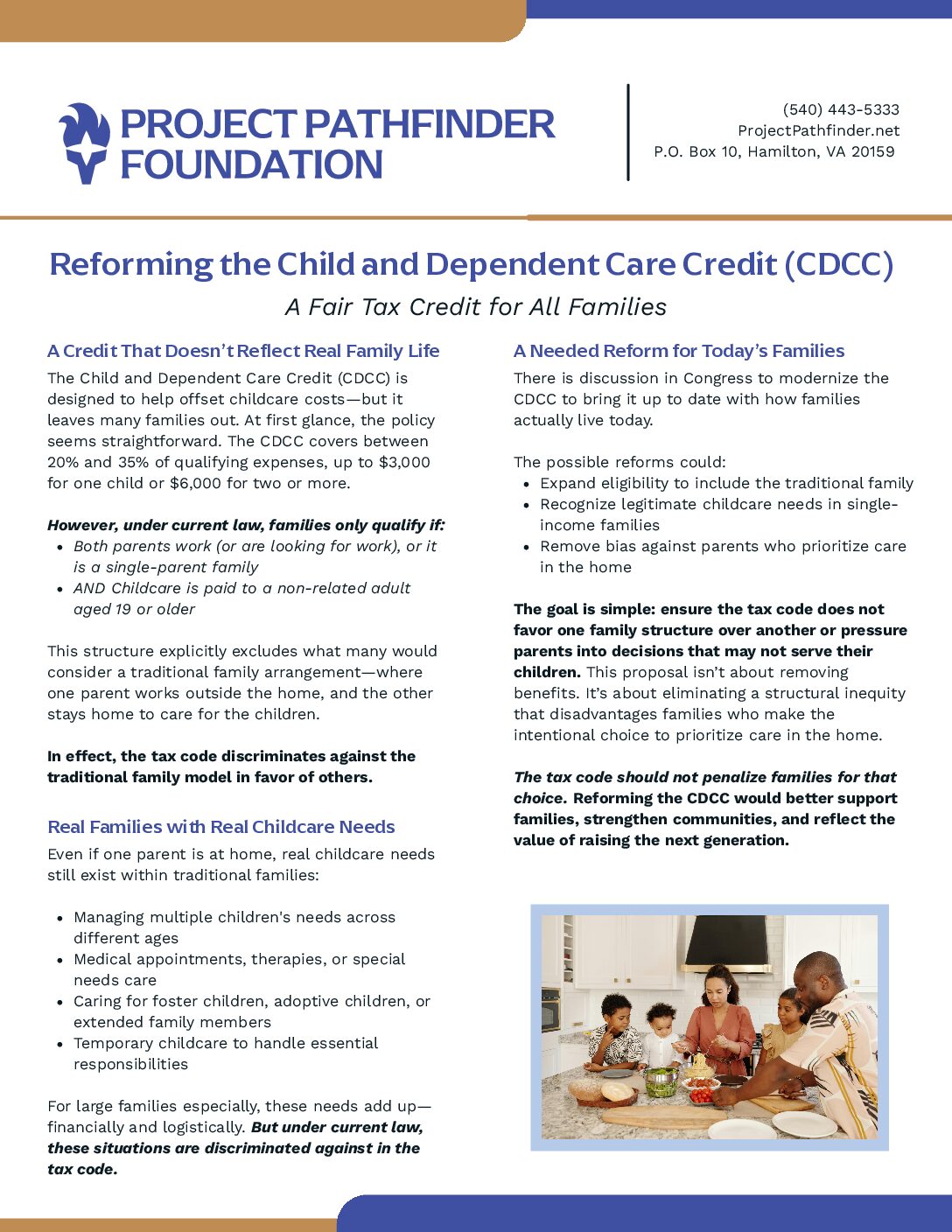

Many single-income families still require regular childcare for a wide range of reasons, reasons that extend far beyond traditional daycare. Consider foster families, for example. Hundreds of thousands across the country open their homes to children in need. In these households, the stay-at-home parent is often responsible for transporting children to court-mandated visits, therapy sessions, and other obligations that cannot be delegated. These responsibilities frequently necessitate additional childcare support.

And foster care is just one example. Medical needs, educational choices, travel requirements, and even caring for aging relatives can all create legitimate and ongoing childcare needs within single-income households. Most of us can think of real-life situations where childcare expenses arise independently of whether both parents are employed.

End the discrimination against families

Recognizing this, there is a proposal in Congress to modernize the CDCC—to bring it in line with how families actually live today. The goal is simple: to ensure that the tax code does not favor one family structure over another or pressure parents into decisions that may not serve the best interests of their children.

The tax code should not penalize families for prioritizing the care of their children. This proposal isn’t about removing existing benefits from anyone. It’s about eliminating a structural discrimination in federal law that leaves certain families at a disadvantage simply because they’ve made a different—and often deeply intentional—choice to prioritize their children, something I think we all could agree society needs more of.

Congress should reform the Child and Dependent Care Credit to remove the discrimination against the traditional family. It’s good for families, good for kids, and good for society at large.